CLICK TO ENLARGE

CLICK TO ENLARGE

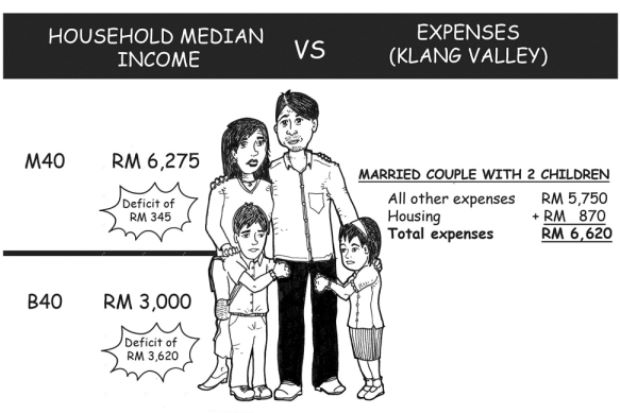

PETALING JAYA: More young property buyers, especially those about to start their own families, may be forced to purchase their first homes in the outskirts of the Klang Valley, such as Rawang and Dengkil, as residential properties in prime city locations suffer from “shrinkflation”.

Shrinkflation refers to the sustained increase in property prices even though new units are smaller than they used to be.

While analysts and industry observers generally welcome Budget 2025’s homeownership measures, the consensus is that more needs to be done because many younger generation workers still find it difficult to buy their first property.

Licensed financial planner Stephen Yong said the supply of affordable housing, particularly in urban areas with manageable commutes, is limited.

ALSO READ: Homes beyond the reach of most M’sians

“Buyers would usually need to save up to 25% of the property’s price to pay for costs like down payment, legal fees, renovations and furnishing – all of which pose a considerable financial burden.

“Young Malaysians also encounter hurdles in securing housing loans due to lower income levels, rising expenses and strict debt service ratio requirements.

“This difficulty is even more pronounced for freelancers and gig economy workers, as banks often impose stricter conditions on applicants without stable, predictable incomes,” said Yong, who is also the executive director of Wealth Vantage Advisory.

The National House Buyers Association (HBA) opined that there is a need to define “affordable housing” to ensure the term is “not abused” by property developers who deem prices of RM500,000 as “affordable”.

ALSO READ: ‘Lock in perks for higher-priced homes’

Its honorary secretary-general Datuk Chang Kim Loong said the government has previously reiterated that affordable housing must meet three criteria: for it to be priced between RM150,000 and RM300,000; must have a minimum built-up of 800sq ft (excluding balcony space) and have at least two bedrooms; and must be located in areas with good public transportation links and amenities.

CLICK TO ENLARGE

CLICK TO ENLARGE

“Whatever schemes are introduced will not make houses affordable if prices are not checked and costs (of doing business) are not addressed.

“Let’s face it, owning a house is beyond the reach of most Malaysians. We need to address the root cause and not pander to parties that caused the hike.

“HBA hopes that the current Housing Minister will always put the interest of the rakyat and country first before the interest of housing developers,” said Chang.

Rahim & Co International Sdn Bhd estate agency chief executive officer Siva Shanker said he welcomes Budget 2025 measures to promote homeownership, especially first-time buyers.

“However, the measures announced are not substantial enough,” he said.

ALSO READ: Tax relief timing for first-time home buyers is crucial

Among the measures announced in Budget 2025 was a RM5bil step-up financing scheme introduced under the Housing Credit Guarantee Scheme (SJKP), which offers a lower repayment rate in the first five years of the mortgage term.

SJKP will also guarantee loans for first-time home buyers of up to RM500,000 for homes developed on wakaf land. To support individuals purchasing their first home, Budget 2025 also proposed an individual tax relief on mortgage interest payments.

There is also a tax relief of up to RM7,000 for residential properties valued up to RM500,000, while a relief of up to RM5,000 will be given for residential properties priced between RM500,000 and RM750,000.

This relief can be claimed for three consecutive years of assessment on sale and purchase agreements completed between Jan 1, 2025, and Dec 31, 2027.

Siva said the real problem affecting first-time homebuyers, especially the bottom 40% income earners (B40), is the difficulty in securing a down payment for the housing loan.

“When you apply for a 90% housing loan but the bank only approves 80%, it means you need a down payment of 20% from the house value. Many people don’t have the cash in hand.

“Perhaps the government can consider a policy where banks will provide 100% loans for first-time B40 homebuyers,” he added.

Malaysian Youth Council executive committee member Eow Shiang Yen said Budget 2025’s step-up financing scheme indicates the government’s commitment to easing the financial burden of the youth.

“However, the success of this scheme requires interactions of other relevant components such as improved financial literacy, building passive and secondary incomes, relevant competence development and competitive salaries,” said Eow.“The youth still need to cope with increasing living costs and other expenses. A strict supervision and ongoing enforcement are also required to ensure that initiatives such as People’s Residency Programmes, People’s Housing Projects, and Rumah Mesra Rakyat are not misused.”

Yong concurred with Eow on the need for financial literacy to make homeownership a reality for young Malaysians.

“In addition, incentives like stamp duty reductions, first-time homebuyer grants, and flexible loan structures with extended tenures would make homeownership more accessible,” he said.

Commenting on the proposed tax relief on mortgage interest payments, Chang said it should be given to all existing homeowners with outstanding housing loans, not just first-time buyers.

The three-year tax relief should start from the date of property handover instead of the date of sale and purchase agreement, he said.

“The tax relief on interests should be applied strictly for first-time buyers irrespective of purchasers from housing developers or from the secondary market or sub-sale,” he added.

Related stories:

Homes beyond the reach of most M’sians

‘Lock in perks for higher-priced homes’

Tax relief timing for first-time home buyers is crucial

Nga: Country on the right track of house ownership

Related posts: